Construction accounting is a specialized form of accounting that tracks costs, revenue, and profitability on a per-project basis rather than at the company level. It accounts for long-term contracts, job costing, progress billing, retainage, and change orders—using methods like the percentage of completion and completed contract method. Because each project functions as its own profit center, construction accounting relies on industry-specific processes and software to ensure accurate reporting, cash flow management, and compliance.

Find a CPA or Bookkeeper for your construction business onSam's List.

Table of Contents

What Is Construction Accounting?

Construction accounting is built specifically for how contractors actually operate: juggling long-term jobs, unpredictable costs, and ever-changing scopes. While it shares the backbone of general accounting, it adds job-centric layers that make traditional tools and approaches fall short.

If you're a contractor and your books just show high-level profit/loss without breaking down job performance, you're likely missing the most important financial signals.

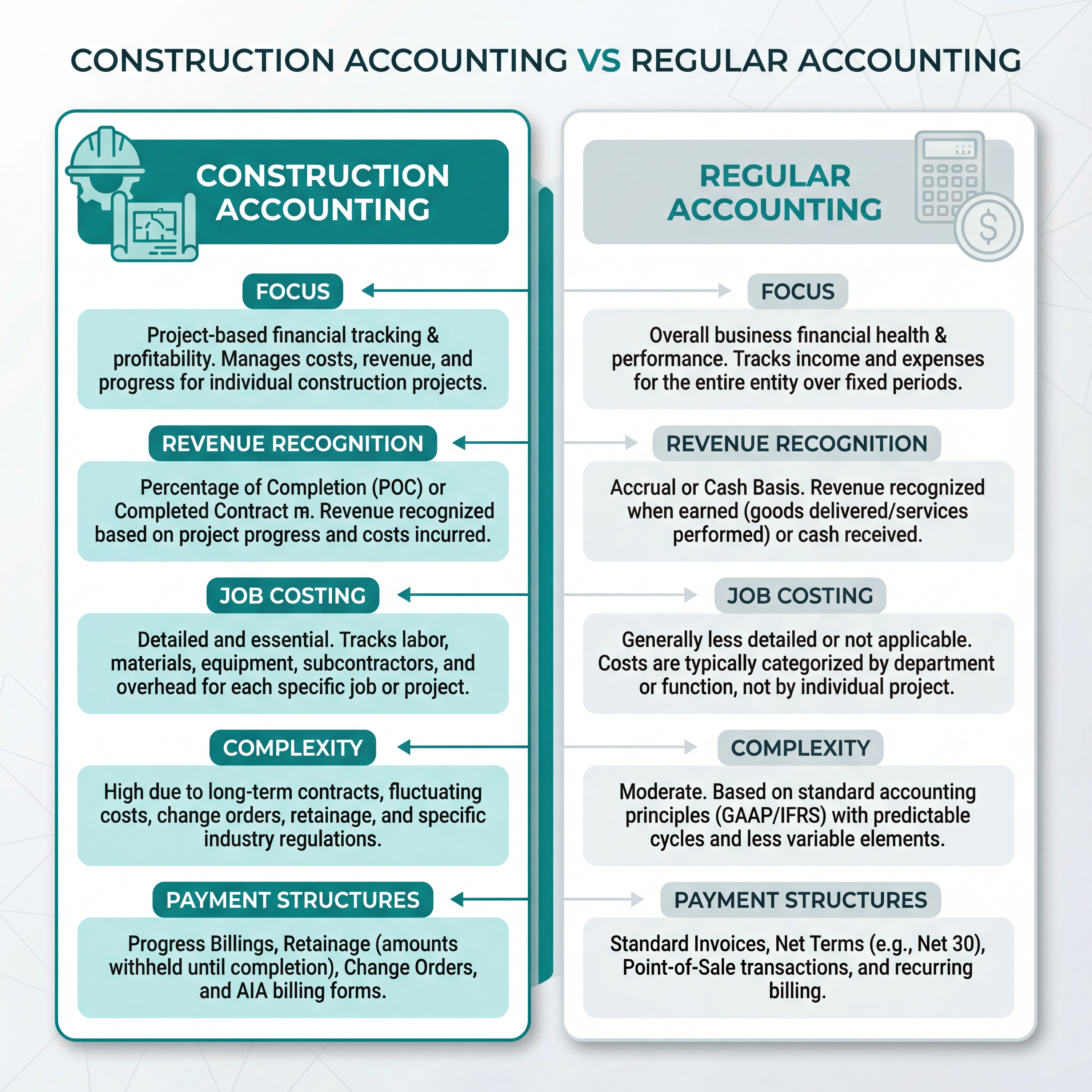

Why Construction Accounting Is Different from Regular Accounting

Project-Based, Not Company-Based

Each job is treated as its own financial universe—its own miniP&L. This lets you understand where you’re making money (or bleeding cash), down to the individual project.

Decentralized Costs Across Sites

From labor to materials to rented equipment, costs are scattered. Construction accounting ties them all back to the right job, phase, and cost code.

Long-Term Contracts & Cash Timing

Cash rarely aligns neatly. You may spend six figures before getting paid. Revenue recognition becomes an art—and a compliance requirement.

| Feature | Traditional Accounting | Construction Accounting |

|---|---|---|

| Focus | Whole business | Each individual project |

| Revenue Recognition | Period-based (monthly) | PCM or CCM methods |

| Labor/Materials Tracking | Generalized | Tracked by job, phase, and crew |

| Software | QuickBooks, Xero | Foundation, Sage 100, Viewpoint |

Core Components of Construction Accounting

Job Costing

The heart of construction accounting.Job costingtracks all costs—labor, materials, subcontractors, equipment, and overhead—against the specific job they belong to. When done right, it lets you:

Monitor budget vs actual in real time

Avoid cost overruns

Bid smarter the next time

Revenue Recognition (PCM vs CCM)

Unlike most industries, construction businesses use:

Completed Contract Method (CCM): Recognize revenue only when a job finishes

Percentage of Completion Method (PCM): Recognize revenue as work is completed

Many usecash accountingfor tax simplicity, but if you want to get bonded or win larger jobs, PCM is often required.

WIP Reports (Work-in-Progress)

WIP reportsare essential for:

Forecasting project profitability

Spotting underbilling/overbilling

Helping bonding agents and lenders assess your financials

What Is Retainage?

Retainage is the portion of payment (usually 5–10%) withheld by the client until a project hits completion or specific milestones. It's meant to ensure quality and completion, but for you—it’s a cash flow killer if not managed.

In your books, it should be tracked separately from accounts receivable, with clear job-level detail.

Why You Can’t Use Standard Accounting Software

General accounting platforms (like Xero or QuickBooks) aren’t designed to handle job costing, certified payroll, or AIA billing.

You need construction-specific tools like:

Foundation

Sage 100 Contractor

Viewpoint

Jonas Premier

NetSuite (Construction Edition)

Why Construction Accounting Matters

Here’s what accurate construction accounting gives you:

📊 Real-time visibility into job profitability

💰 Better control over cash flow

🧾 Compliance with bonding and tax rules

📈 Smarter, data-backed bids

🔍 Evidence that keeps lenders and investors confident

If you’re not doing project-level tracking and regular WIP reports, you’re guessing—not managing.

When You Need a Construction CPA

If your current accountant doesn’t:

Understand WIP reports or retainage

Help you evaluate PCM vs CCM

Know how to prep for bonding audits

Work with Foundation or Sage...

...you probably need a new accountant.Sam’s Listcan connect you with vetted construction CPAs who know your world.

FAQs About Construction Accounting

What type of accounting is used in construction?

Most companies use the percentage-of-completion method, especially for longer projects, since it recognizes revenue as work is completed.

Is construction accounting difficult?

Yes—it’s more complex than standard accounting due to job-based tracking, delayed revenue, and specialized compliance requirements.

How is construction accounting different from regular accounting?

It’s project-based, not just company-wide. It also uses specialized methods like PCM and WIP tracking to manage long-term contracts and cash flow.

What is GAAP in construction accounting?

GAAP (Generally Accepted Accounting Principles) in construction governs how you recognize revenue (e.g., ASC 606), prepare financials, and ensure consistency across reporting.

Ready to Get Help?

If you’re running a construction company and your books don’t make sense—don’t wing it.Sam’s Listcan connect you with:

Click here to find your expert now.

Written by Kimberly Green, cofounder of Sam's List | kimi@samslist.co

Last updated: December 20, 2025